Updated: February 2026

China remains the world’s largest producer and exporter of tilapia. The 2024–2025 period marked a full market cycle — from record-high prices to structural adjustment under global trade pressure. Entering 2026, the industry is transitioning into a new supply-demand balance phase.

This report summarizes China tilapia price trends, export performance and 2026 outlook for global seafood buyers.

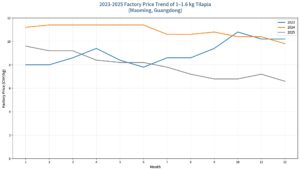

China Tilapia Price Trend (2024–2025)

In 2024, strong international demand pushed farm-gate prices to a 20-year high. In Guangdong’s key production area (Maoming region), factory purchase prices for 500–800g whole tilapia reached approximately RMB 5.7 per jin during peak months.

However, in 2025, higher import duties in major overseas markets significantly increased export costs and reduced pricing competitiveness.

Price movement summary:

-

2024 Q1–Q2: Historical peak levels

-

2024 Q3–Q4: Moderate correction with new harvest supply

-

2025 H1: Prices remained above RMB 4/jin

-

2025 H2: Decline to RMB 3.2–3.6/jin range

By late 2025, many farmers faced margin pressure, leading to reduced fry stocking and lower 2026 production expectations.

2025 China Tilapia Export Data

According to China customs statistics:

-

Total export volume: 519,700 metric tons

-

Total export value: USD 1.216 billion

-

Main markets: United States, Mexico, West Africa

Top exported product categories:

-

Prepared or preserved tilapia (whole or cuts)

-

Frozen whole tilapia

-

Frozen tilapia fillets

Exports to the United States totaled approximately USD 350 million in 2025, representing a year-on-year decline compared to 2024.

Despite volume resilience, average export unit prices declined throughout 2025, especially in Q4, reflecting weaker premium margins in international markets.

South China Production Analysis

Guangdong, Hainan and Guangxi remain the core tilapia production regions.

Combined export volume from these three provinces reached approximately 415,000 metric tons in 2025.

Based on processing yield rates (45%–55%), this corresponds to raw material demand of approximately 750,000–910,000 metric tons.

Estimated total national production in 2025:

1.45–1.7 million metric tons

(compared to approximately 1.8 million metric tons in 2024)

This suggests a moderate production contraction due to reduced profitability.

2026 Supply Outlook

Several factors will influence China tilapia supply in 2026:

-

Reduced fry stocking in early 2026

-

Lower pond inventory entering the year

-

Processing plant capacity adjustments

-

Global demand stabilization

While short-term supply-demand imbalance remains, reduced production may gradually support price stabilization later in 2026.

For international buyers, the market is entering a phase of more flexible pricing and stronger negotiation leverage compared to the 2024 peak period.

What This Means for Global Tilapia Importers

China continues to offer:

-

Large-scale integrated farming and processing

-

Competitive frozen tilapia fillet production

-

Flexible private label solutions

-

Stable export logistics infrastructure

At CHF Seafood, we closely monitor raw material availability, processing efficiency and export trends to provide consistent supply and transparent pricing strategies for our partners.

For updated quotations, frozen tilapia specifications, or customized packaging solutions, please contact our sales team.

For more details on our tilapia products, please visit our Frozen Tilapia Product Page.